You'll be re-directed to the Financial Professional site.

The opportunity in emerging markets (EM) is vast and expanding. EM comprise over 85% of the world’s population and have contributed 52% of global GDP1 growth since 2000.

Economic growth in EM has outpaced that of developed markets over the past two decades, and we believe this trend will persist. EM are benefiting from advancements in education and technology, which have bolstered productivity. More market-friendly policies have created favourable environments for businesses and investors. Positive demographic trends, such as larger middle-class populations, and rising urbanisation are fueling demand for various goods and services. Companies that strategically tap into these burgeoning markets should reap significant rewards. Given their immense potential for growth and development, EM offer fertile ground for innovation, investment, and economic development.

As EM have grown in importance, their weight within major global indices has also increased. For example, the MSCI Emerging Markets Index (MSCI EM) as a percentage of the MSCI ACWI Index is now 2.4 times larger than it was in 2000.2 Moreover, MSCI’s definition of EM continues to evolve, incorporating new countries into the fold, reflecting an expanded universe of investable opportunities. The MSCI EM currently includes 24 countries versus only 10 at the Index’s inception.

Despite their increasing prominence, EM equities remain underrepresented relative to their economic significance. The MSCI EM represents 11% of the MSCI ACWI, yet companies based in EM or whose businesses largely serve EM3 comprise 30% of total global market capitalisation.

EM Performance: A Tale of Three Periods

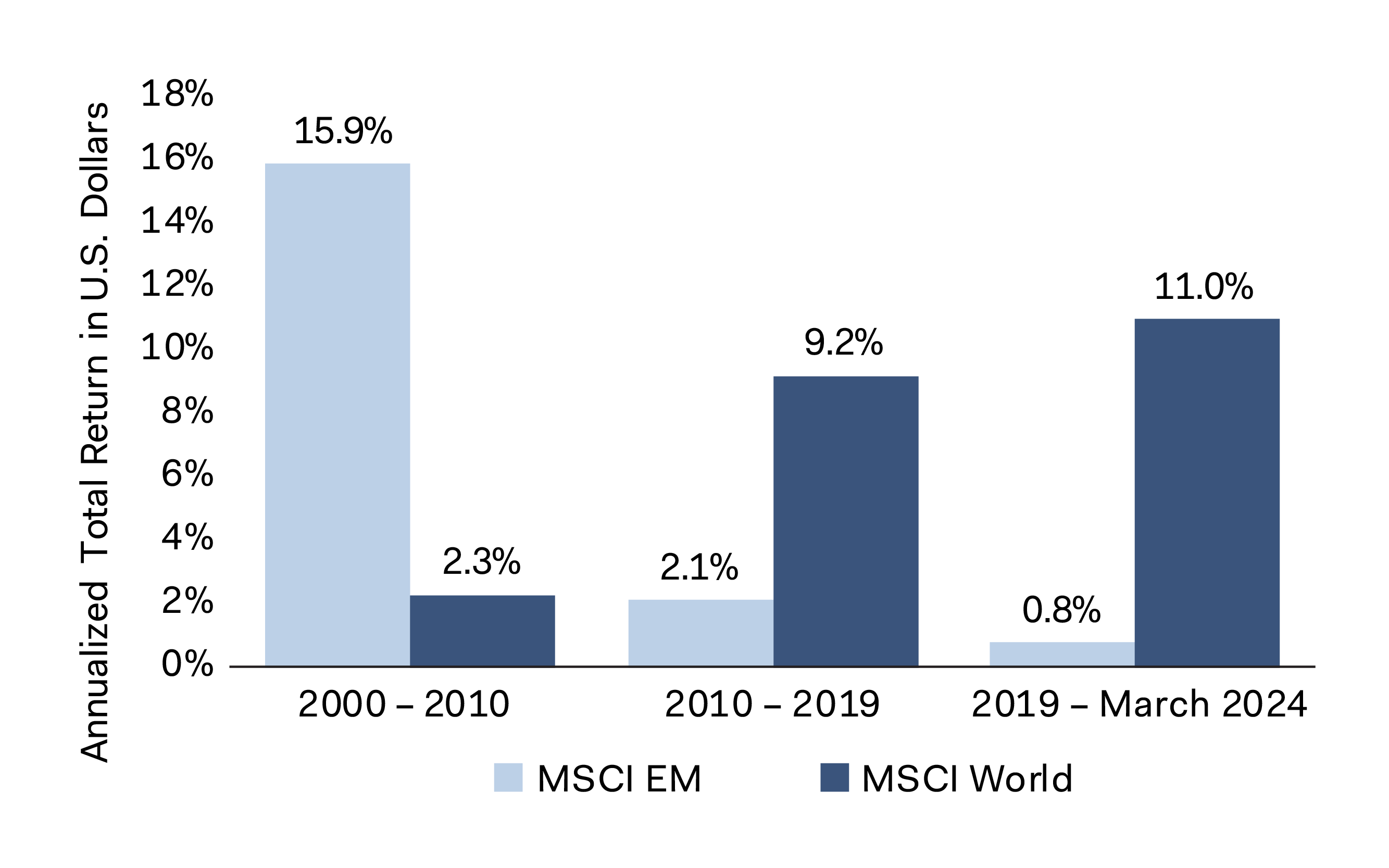

Given the economic growth in EM, how have EM equities performed since 2000? As shown in Figure 1, EM significantly outperformed developed markets (represented by the MSCI World Index)4 from December 2000 to 2010, but have underperformed since then. Here’s why:

- December 2000 to December 2010: EM companies had exceptionally strong sales growth that outpaced developed markets. Consumer demand drove growth across various sectors and attracted significant inflows into EM equities.

- December 2010 to December 2019: After the global financial crisis, many EM economies expanded. However, EM underperformed due to margin compression, currency headwinds, and a lack of multiple expansion.5

- December 2019 to March 2024: The COVID-19 pandemic disproportionately harmed EM, resulting in their significant underperformance during and after the pandemic. Increasing global geopolitical tensions, China's struggling economy, the dominance of a few U.S. technology giants (known as the Magnificent Seven),6 and less direct exposure to transformative technologies (e.g., artificial intelligence) further widened the performance gap.

Figure 1. MSCI EM Outperformed Significantly in 2000-2010

Source: MSCI. Returns are in U.S. dollars.

EM Equity: An Attractive Asset Class

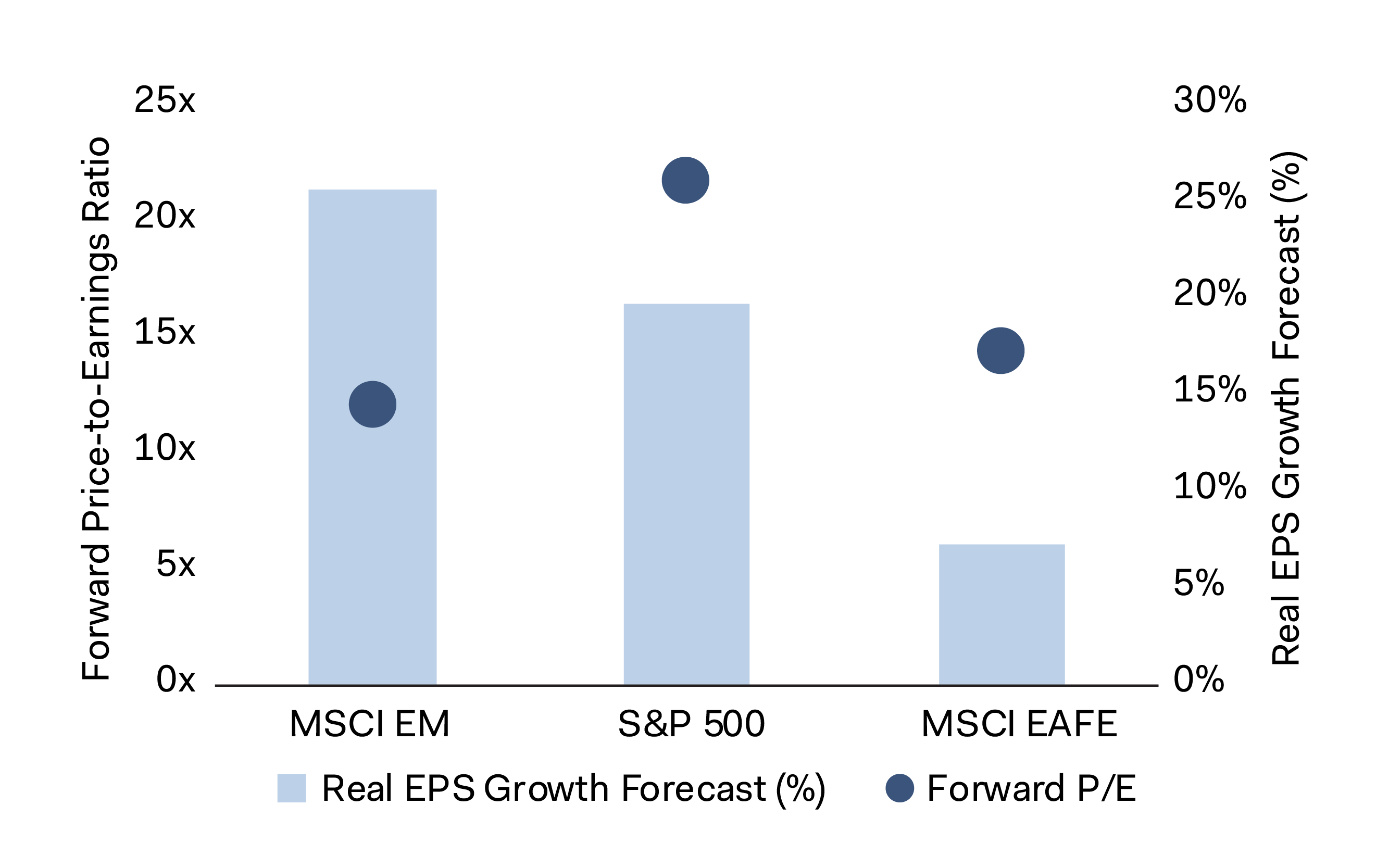

As a result of recent underperformance, EM companies are collectively trading at relatively inexpensive valuations, as illustrated in Figure 2. Importantly, they also have attractive earnings growth7 prospects. Earnings growth in EM is expected to be higher in both absolute and relative terms compared to growth in the United States and other developed markets. On 31 March, the MSCI EM traded at 12.1 times forward earnings, compared to 21.7 times for the S&P 500 Index and 14.3 times for the MSCI EAFE Index.8 Starting valuations matter—lower starting valuations can provide a margin of safety. Having a long-term investment horizon and analysing securities on a bottom-up basis also helps investors identify compelling opportunities.

There are risks to consider when investing in EM, including greater political instability, less established legal and regulatory regimes, and currency fluctuations. Nevertheless, the combination of attractive valuations, robust growth prospects, and potential diversification benefits (discussed below) make EM equities an appealing asset class for long-term investors.

Figure 2. EM: Inexpensive with Higher Growth Prospects

Source: FactSet, MSCI.

EM Exposure May Improve Risk-Adjusted Returns

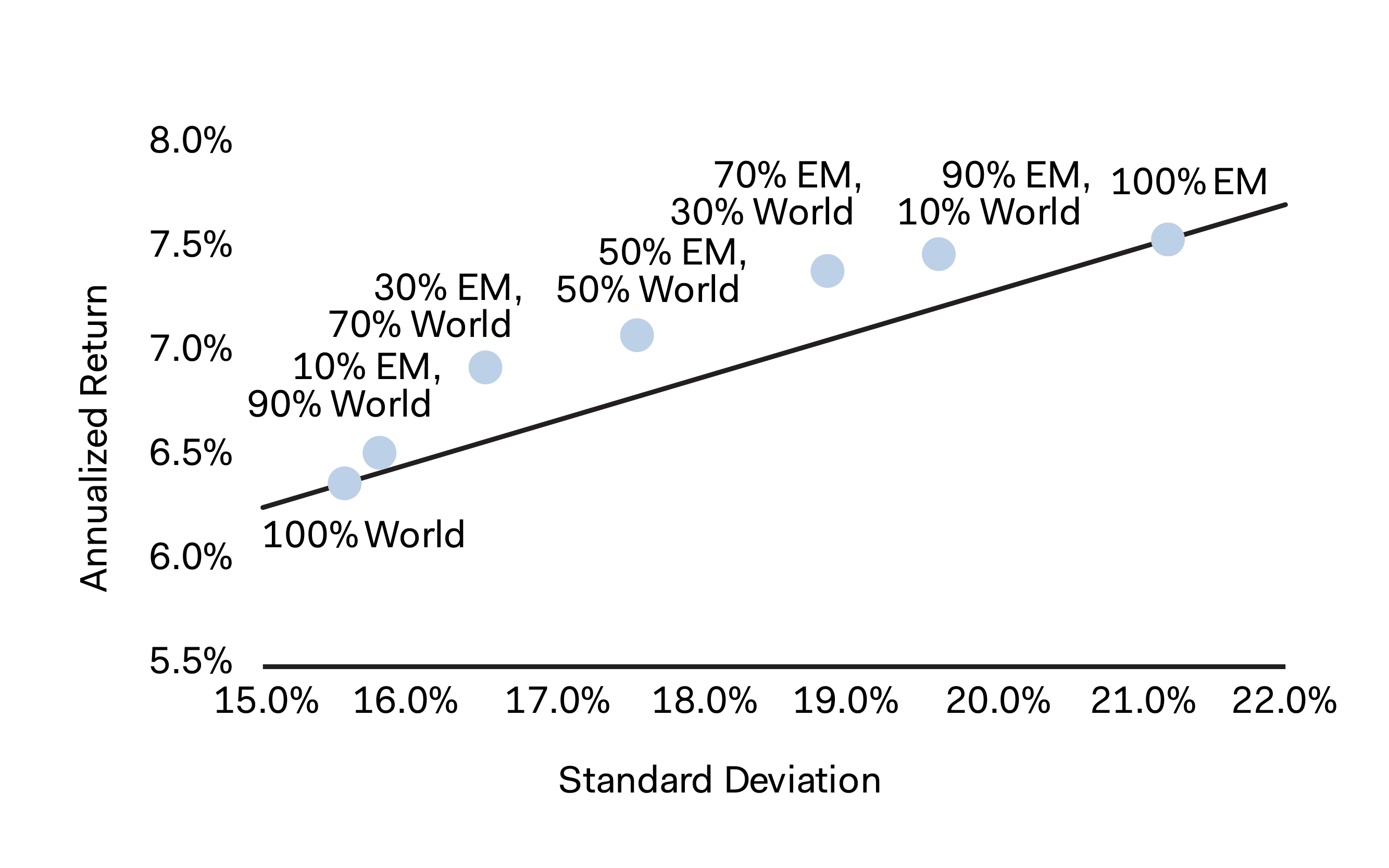

EM equities offer unique opportunities and risks that can complement a diversified portfolio. Investing in EM is typically considered riskier than investing in developed markets. Indeed, since 2000, the MSCI EM has been more volatile than the MSCI World, using the standard deviation9 of monthly returns as a proxy for volatility. Over the same period, the MSCI EM generated higher returns than the MSCI World. That may not be surprising.

However, a portfolio reflecting a blend of emerging and developed markets indices would have generated higher returns than a developed markets-only portfolio, with only a small increase in volatility. Figure 3 shows the performance of various blends of the MSCI EM and MSCI World Indices. These returns illustrate the important role that EM equities can play in a portfolio.

Figure 3. Average Annual Total Return of Portfolios of MSCI EM and MSCI World Rebalanced Monthly (1999 through March 31, 2024)10

Source: Bloomberg, MSCI. Past performance is no guarantee of future results. Index returns include dividends, but unlike Fund returns, do not reflect fees or expenses. Returns are in U.S. dollars.

Small-Cap EM: Greater Diversification and Market Inefficiencies

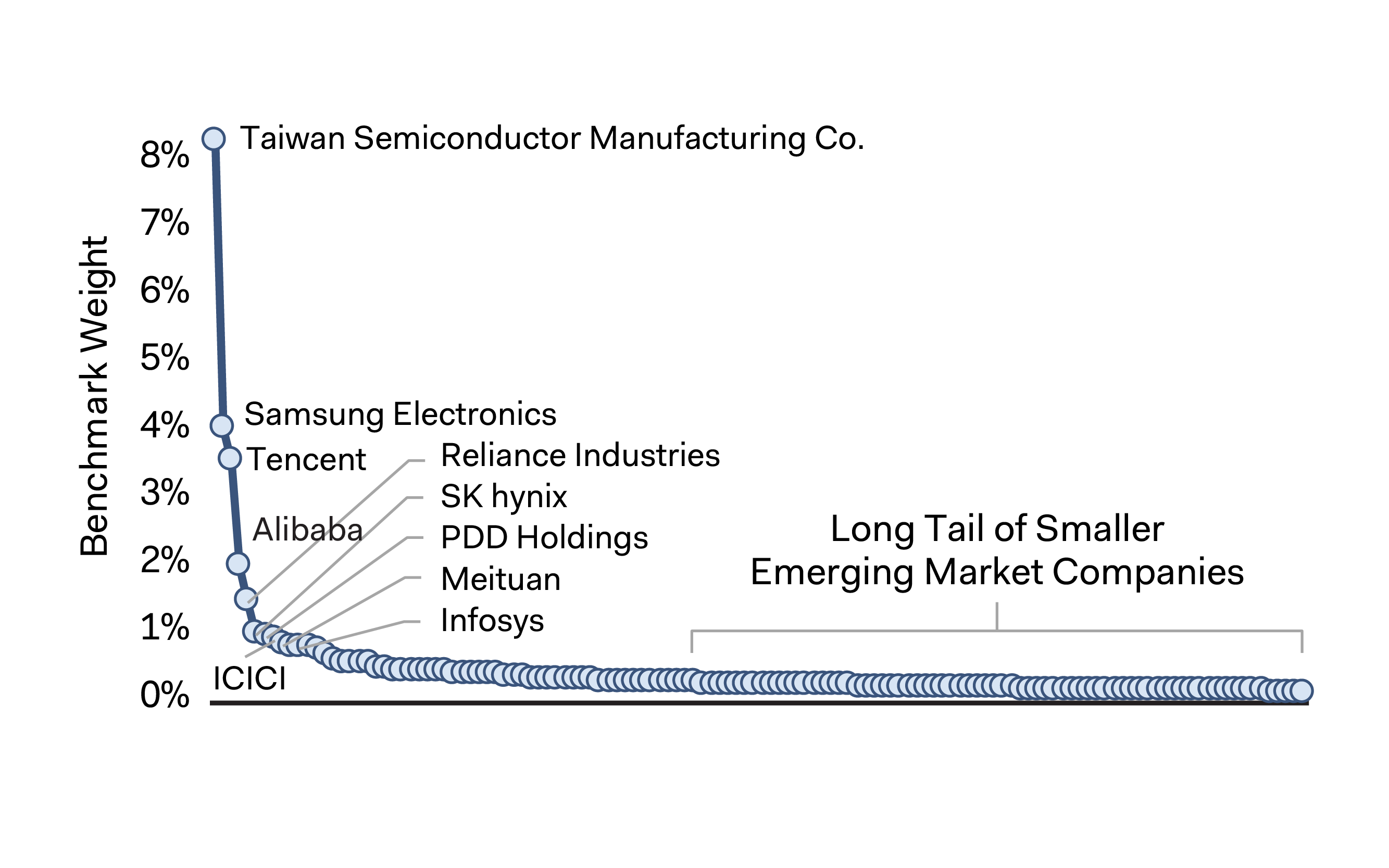

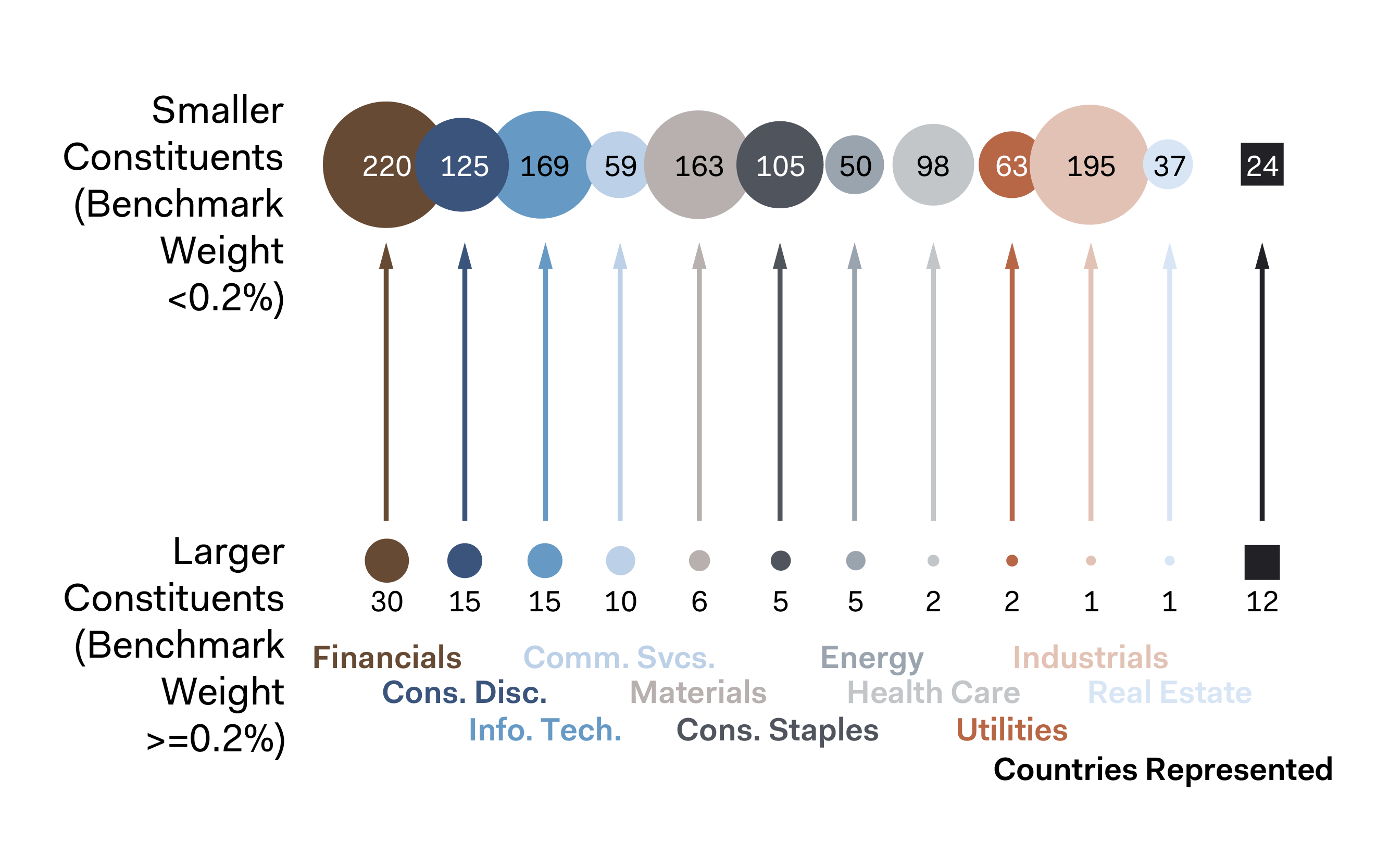

Smaller companies often operate in niche markets or serve local needs, providing a different risk-return profile from larger, more globally oriented firms. As shown in Figure 4, 69% of the MSCI EM’s constituents are less than 0.05% positions (versus 34% of the S&P 500 and 45% of the MSCI EAFE). Investing in this long tail of smaller EM companies can help spread risk across a broader spectrum of industries and regions. For example, in the Industrials sector, there is only one larger company that has a weight greater than 0.20% in the MSCI EM, but there are 195 smaller companies with weights less than 0.20% (see Figure 5).

Figure 4. MSCI EM Constituents11

Source: MSCI.

Figure 5. MSCI EM Constituent Count by GICS Sector & Country

Source: MSCI.

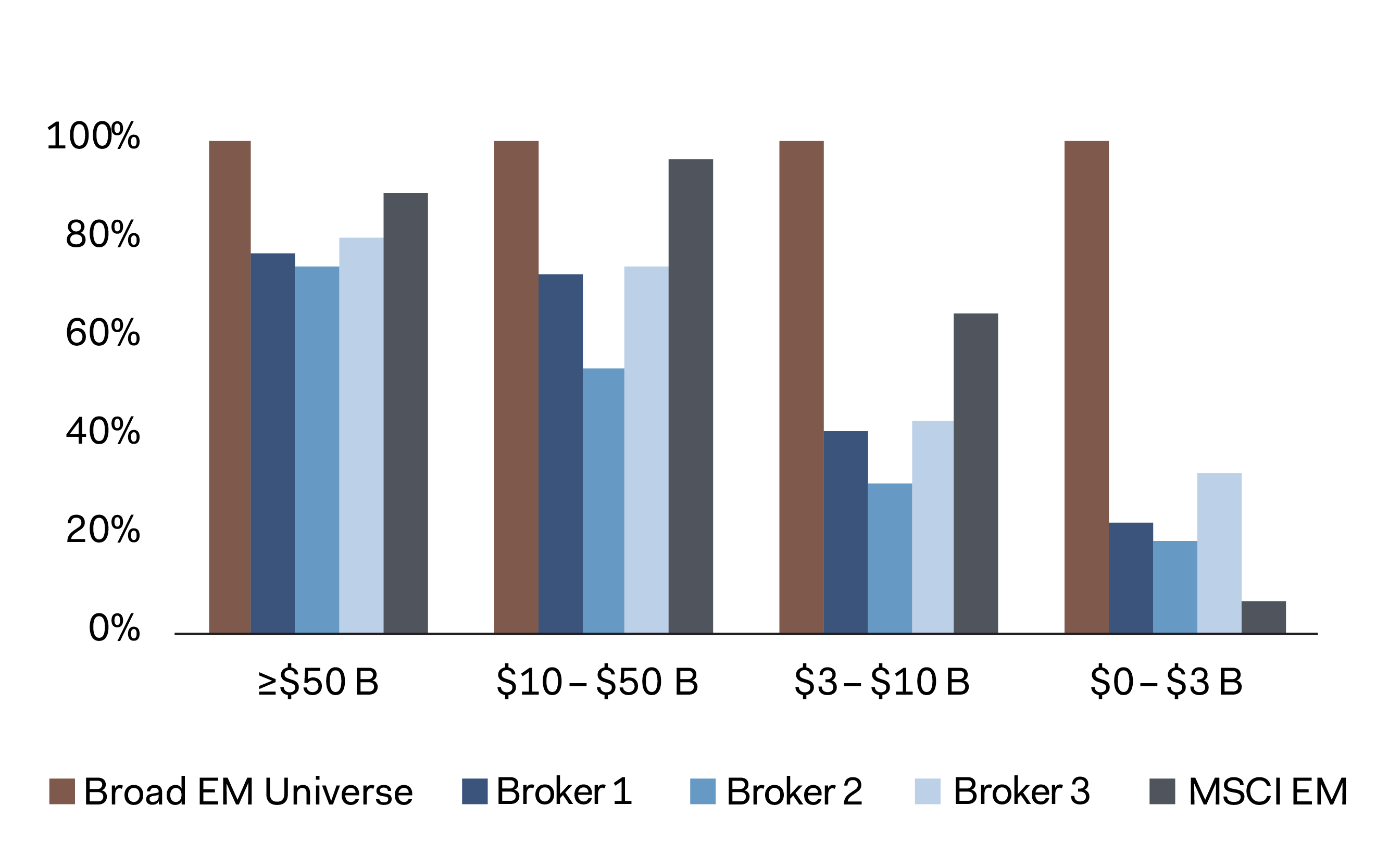

The broad EM universe3 is approximately three times larger than the MSCI EM. As market capitalisations decrease, sellside equity research coverage and MSCI EM exposure tend to drop off dramatically (see Figure 6). Smaller companies often fly under the radar of sell-side analysts, and their valuations can be attractive. The smallest 80% of MSCI EM constituents by weight trade at a 15% discount12 to the largest 20%. By tapping into these market inefficiencies, investors can potentially capture higher returns while simultaneously diversifying their portfolios, making smaller EM companies an attractive proposition for those seeking to optimise risk-adjusted returns.

Figure 6. Thinner Broker Coverage Suggests Potential for Market Mispricing/Inefficiencies

Sell-Side Coverage as a % of Broad EM Investable Universe by Market Cap

Source: FactSet, MSCI.

Interested in Hearing More?

EM equities can provide exposure to thriving economies, low valuations, attractive earnings growth prospects, diversification benefits, and potentially higher risk-adjusted returns. We welcome the opportunity to discuss our active, value-oriented approach to investing in EM.

Contributors

Disclosures

This information should not be considered a solicitation or an offer to purchase shares of Dodge & Cox Worldwide Funds plc or a solicitation or an offer by Dodge & Cox Worldwide Investments Ltd. and its affiliates to provide any services in any jurisdiction. A summary of investor rights is available in English at dodgeandcox.com. Dodge & Cox Worldwide Funds plc are currently registered for distribution in Austria, Denmark, Finland, France, Germany, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, South Africa, Spain, Sweden, Switzerland, and the United Kingdom. The Funds may terminate the arrangements made for the marketing of any fund or share class in an EU Member State at any time by using the process contained in Article 93a of the UCITS Directive.

This is an advertising document. First Independent Fund Services AG, Klausstrasse 33, CH-8008 Zurich, is the representative in Switzerland and NPB Neue Privat Bank AG, Limmatquai 122, CH-8024 Zurich, is the paying agent in Switzerland. The sales prospectus, key investor information, copies of the articles of association and the annual and semi-annual reports of the fund can be obtained free of charge from the representative in Switzerland.

Marketing Communication. The views expressed herein represent the opinions of Dodge & Cox Worldwide Investments and its affiliates and are not intended as a forecast or guarantee of future results for any product or service. Please refer to the Funds’ prospectus and relevant key information document at dodgeandcox.com before investing for more information, including risks, charges, and expenses, or call +353 1 242 5411.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed, or produced by MSCI. The S&P 500 Index (“Index”) and associated data are a product of S&P Dow Jones Indices LLC, its affiliates and/or their licensors and has been licensed for use by Dodge & Cox. © 2023 S&P Dow Jones Indices LLC, its affiliates and/or their licensors. All rights reserved.

Endnotes

1. Unless otherwise specified, all weightings and characteristics are as of 31 March 2024. Gross domestic product (GDP) measures the monetary value of final goods and services—those that are bought by the final user—produced in a country in a given period of time. It counts all of the output generated within the borders of a country. GDP is composed of goods and services produced for sale in the market and also includes some non-market production, such as defence or education services provided by the government.

2. The MSCI Emerging Markets Index captures large- and mid-cap representation across emerging market countries. The MSCI ACWI (All Country World Index) Index is a broad-based, unmanaged equity market index aggregated from developed market and emerging market country indices.

3. In determining whether an issuer is located in or has significant economic exposure to an emerging market country, Dodge & Cox will consider the issuer’s country of organisation, the location of its management, the country of its primary listing, its reporting currency, and whether the issuer has significant assets in, or derives significant revenues or profits from, emerging market countries.

4. The MSCI World Index is a broad-based, unmanaged equity market index aggregated from developed market country indices, including the United States. It covers approximately 85% of the free float-adjusted market capitalisation in each country.

5. Multiple expansion means that investors were willing to pay more for the same amount of earnings.

6. The “Magnificent Seven” stocks are Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA, and Tesla.

7. Earnings growth is the percentage change in a firm's earnings per share (EPS) in a period, as compared with the same period from the previous year.

8. Price-to-earnings (forward) ratios are calculated using 12-month forward earnings estimates from third-party sources as of the reporting period. Estimates reflect a consensus of sell-side analyst estimates, which may lag as market conditions change. The S&P 500 Index is a market capitalisation-weighted index of 500 large-capitalisation stocks commonly used to represent the U.S. equity market. The MSCI EAFE (Europe, Australasia, Far East) Index is a broad-based, unmanaged equity market index aggregated from developed market country indices, excluding the United States and Canada. It covers approximately 85% of the free float-adjusted market capitalisation in each country.

9. Standard deviation measures the volatility of the Fund’s returns. Higher Standard Deviation represents higher volatility.

10. Performance data for the MSCI Emerging Markets Net Total Return USD Index is first available in Bloomberg starting on 31 December 1998. As a result, the first annual period of performance begins on 31 December 1999.

11. The chart shows the top ten constituents in the MSCI Emerging Markets Index as of 31 March 2024.

12. Calculated based on an average of the discounts for three metrics: trailing price-to-earnings, price-to-sales, and price-to-book ratios.