You'll be re-directed to the Financial Professional site.

The exceptional performance of a handful of high-valuation technology companies has led investors to question the merits of value investing. When Morningstar recently sat down with David Hoeft, they concluded, “value investing is alive and well.” We expand upon their conversation and share why we believe our approach is well suited to capture opportunities in today's bifurcated market environment.

Value Investing: A Look Back

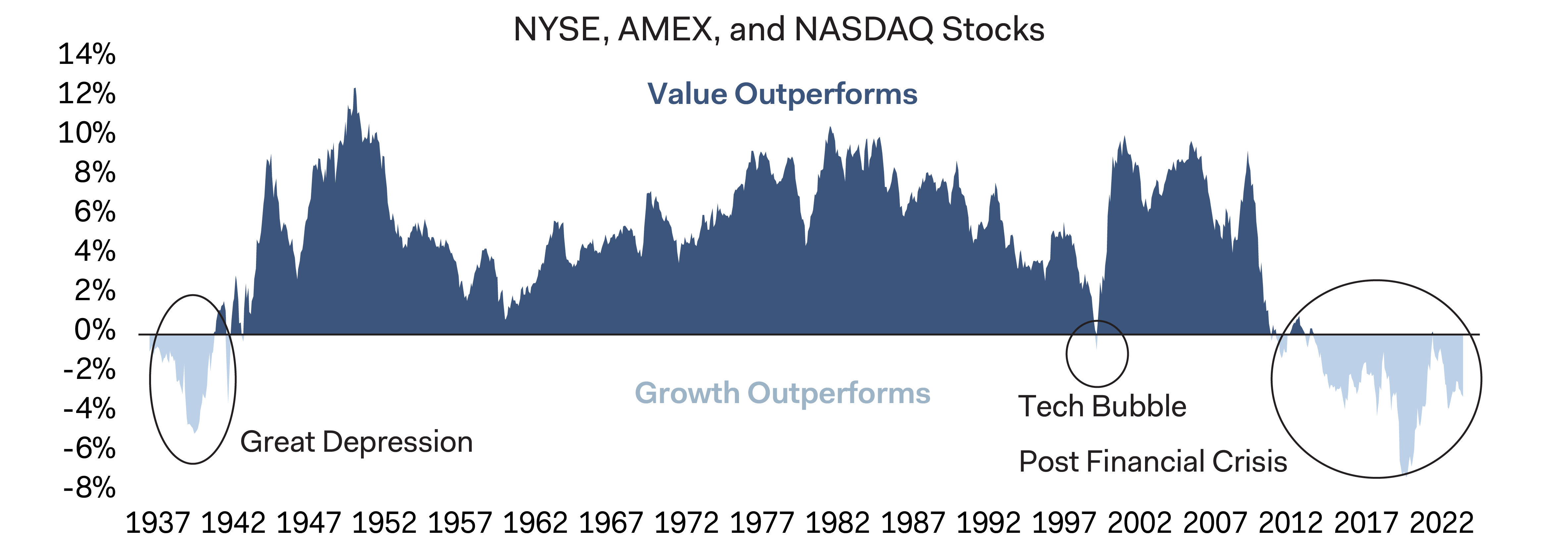

Value investing has stood the test of time despite periodic challenges and shifting market dynamics. Over shorter periods, the relative performance of growth and value stocks1 has seesawed, but value strategies have nearly always outperformed over horizons of a decade or more (see Figure 1). In fact, there have been only three periods over the past 90+ years when value stocks have underperformed on a rolling ten-year basis in the United States: the Great Depression, the Technology Stock Bubble, and after the Global Financial Crisis.

Figure 1. Rolling 10-Year Total Return Difference: Fama-French HML (Value vs. Growth)2

Source: Kenneth French’s Data Library.

The past decade was an especially strong period for growth stocks: the Russell 1000 Growth Index outperformed the Russell 1000 Value Index by 233 percentage points.3 Given their strong performance, the “Magnificent Seven” stocks—Alphabet, Amazon, Apple, Microsoft, Meta Platforms, NVIDIA, and Tesla—accounted for 45% of the Russell 1000 Growth Index’s total return. The Magnificent Seven now represent a staggering 52% of the Russell 1000 Growth and 32% of the S&P 500 Index.4

Why the Next Decade Should be Better for Value

S&P 500: Valuations Are High with Unrealistic Expectations

On an absolute basis, the U.S. equity market is expensive, trading at 21.6 times forward earnings, and 18.2 times if you exclude the Magnificent Seven.5 We’re concerned that market expectations for earnings growth6 are too high. The S&P 500’s 2023-2026 earnings-per-share growth is estimated to be 12.4%. However, the S&P 500 hasn’t managed to grow earnings that quickly over a three-year period in the past 35 years without starting from a depressed base, which we clearly don’t have today. Operating income (EBIT7) margins are 17.7% today—also very high by historical standards—so we’re not thrilled at the prospect of paying a historically high multiple on historically high margins. In contrast, the value-oriented Dodge & Cox Worldwide Funds — U.S. Stock Fund trades at an attractive 14.0 times forward earnings.

Valuation Disparities Are Wide

The Magnificent Seven’s exceptional performance has caused valuation spreads to widen considerably. The most expensive quartile of the S&P 500 trades at 36.2 times forward earnings, compared to 10.5 times for the least expensive quartile.

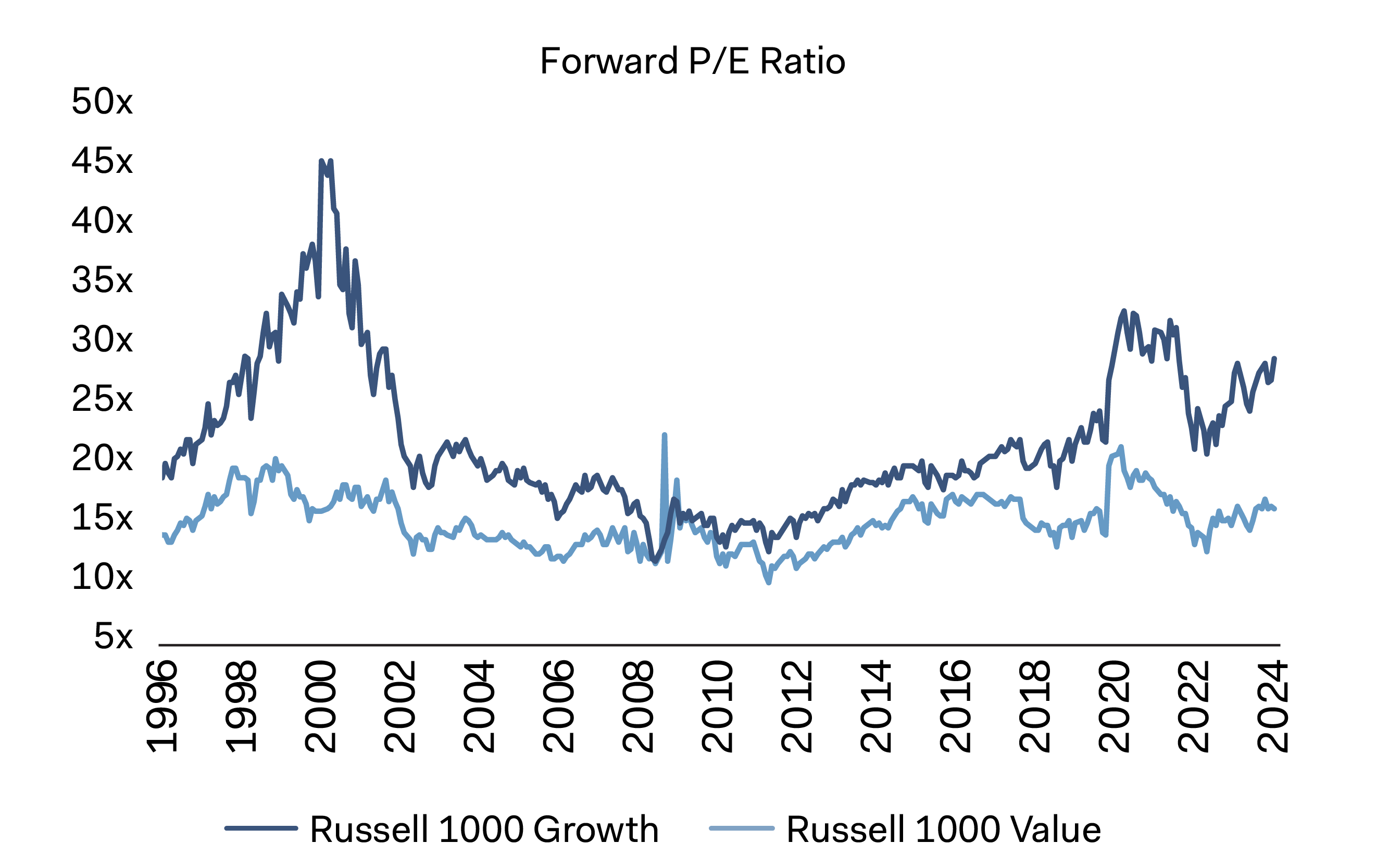

Similarly, the Russell 1000 Growth trades at 28.8 times forward earnings versus 16.1 times for the Russell 1000 Value (see Figure 2). The valuation gap between these groups of stocks remains wide at 2.1 standard deviations,8 with value stocks less expensive than they have been nearly 95% of the time since 1995.

Figure 2. Rising Valuations with Wider Growth/Value Spread

Source: Bloomberg Index Services, Russell.

A compression of this massive spread would be a substantial tailwind for value investing. Historically, strong relative returns for value-focused strategies have been closely related to valuation spreads.

Outside the United States, the valuation disparity between value and growth stocks is also dramatic: the MSCI ACWI ex USA Value Index trades at 10.0 times compared to 20.0 times for the MSCI ACWI ex USA Growth Index.9 This gap now stands at 1.6 standard deviations, in the 84th percentile of historical observations.

Large Magnitude of Potential Opportunities

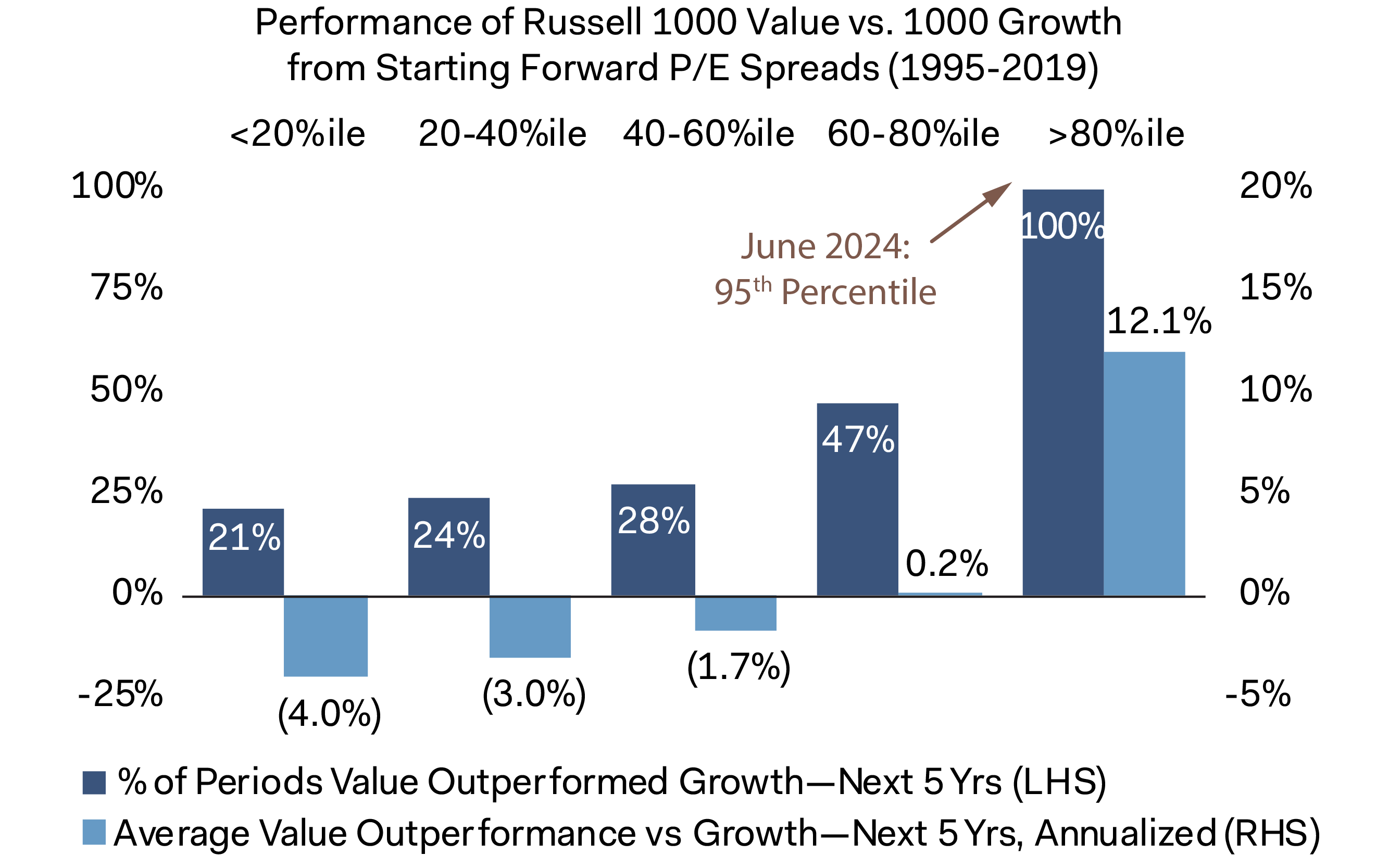

Historically, the Russell 1000 Value has outperformed the Russell 1000 Growth for every 5-year period when the valuation spread has been wider than the 80th percentile (see Figure 3). On June 30, 2024, this spread was in the 95th percentile.

Figure 3. Wide Spreads Have Been Positive for Value

Source: Bloomberg Index Services, FactSet, Russell.

When low valuation companies have been in the cheapest 20% of the range versus expensive companies since 1995 (like they are today), the Russell 1000 Value has outperformed by over 12% per year when annualized for five years. Valuation isn't prescriptive, especially when you look at short-term time horizons. But if you take a longer-term view of 5 to 10 years, the power of relative valuation to predict performance goes up substantially, so it pays to have a long-term horizon.

What Value Investing Means to Dodge & Cox

Value investing isn't just about finding companies with low prices, it's thinking creatively about the underlying value of the business. For instance, just buying low-priced stocks isn't a viable long-term investing strategy if you don't have more holistic insight into intangibles and other sources of value that may not show up directly on the balance sheet. Intangible assets—such as goodwill, intellectual property, and brand strength—can prove valuable for a firm and critical to its long-term success or failure.

Our investment team considers broad sources of value—tangible and intangible—to identify potential opportunities and risks, which inform our return scenarios. We assess the individual dynamics of each company and tailor our valuation analysis, utilizing an array of sophisticated, industry-specific metrics for each company. Valuation is the yardstick of the gap between price and value.

The current growth/value spread has created a compelling environment. We think now is an interesting time for value investors, and we're particularly enthusiastic about the long-term prospects for our approach to value investing.

Contributors

Disclosures

This information should not be considered a solicitation or an offer to purchase shares of Dodge & Cox Worldwide Funds plc or a solicitation or an offer by Dodge & Cox Worldwide Investments Ltd. and its affiliates to provide any services in any jurisdiction. A summary of investor rights is available in English at dodgeandcox. com. Dodge & Cox Worldwide Funds plc are currently registered for distribution in Austria, Denmark, Finland, France, Germany, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, South Africa, Spain, Sweden, Switzerland, and the United Kingdom. The Funds may terminate the arrangements made for the marketing of any fund or share class in an EU Member State at any time by using the process contained in Article 93a of the UCITS Directive.

This is an advertising document. First Independent Fund Services AG, Klausstrasse 33, CH-8008 Zurich, is the representative in Switzerland and NPB Neue Privat Bank AG, Limmatquai 122, CH-8024 Zurich, is the paying agent in Switzerland. The sales prospectus, key investor information, copies of the articles of association and the annual and semi-annual reports of the fund can be obtained free of charge from the representative in Switzerland.

Marketing Communication. The views expressed herein represent the opinions of Dodge & Cox Worldwide Investments and its affiliates and are not intended as a forecast or guarantee of future results for any product or service. Please refer to the Funds’ prospectus and relevant key information document at dodgeandcox.com before investing for more information, including risks, charges, and expenses, or call +353 1 242 5411.

London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). © LSE Group 2023. FTSE Russell is a trading name of certain of the LSE Group companies. “Russell®” is/are a trademark(s) of the relevant LSE Group companies and is used by any other LSE Group company under license. All rights in the FTSE Russell indexes or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company’s express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The S&P 500 Index (“Index”) and associated data are a product of S&P Dow Jones Indices LLC, its affiliates and/or their licensors and has been licensed for use by Dodge & Cox. © 2023 S&P Dow Jones Indices LLC, its affiliates and/or their licensors. All rights reserved. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed, or produced by MSCI.

Endnotes

1. Generally, stocks that have lower valuations are considered “value” stocks, while those with higher valuations are considered “growth” stocks.

2. Monthly observations, data ends April 2024 (latest available at time of publication). Calculated based on data from Kenneth French’s website (http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/index.html), which was derived from the CRSP (Center for Research in Security Prices)/COMPUSTAT merged database. CRSP recently completed a data series project that added new daily data, which resulted in changes to month-end prices and dividend ex-dates and also changed historical returns on French’s website. This chart includes the restated data as of 31 July 2017. High minus Low (HML) is one of three factors in the Fama-French model and accounts for the spread in returns between value and growth stocks. The Fama-French portfolios used to calculate the chart above include all NYSE, AMEX, and NASDAQ firms with the necessary data.

3. For the 10-year period ended 30 June 2024, the Russell 1000 Growth Index had a total return of 353.74%, compared to 120.16% for the Russell 1000 Value Index. The Russell 1000 Growth Index is a broad-based, unmanaged equity market index composed of those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values. The Russell 1000 Value Index is a broad-based, unmanaged equity market index composed of those Russell 1000 companies with lower price-to-book ratios and lower forecasted growth values.

4. Unless otherwise specified, all weightings and characteristics are as of 30 June 2024. The S&P 500 Index is a market capitalisation-weighted index of 500 large-capitalisation stocks commonly used to represent the U.S. equity market.

5. Price-to-earnings (forward) ratios are calculated using 12-month forward earnings estimates from third-party sources as of the reporting period. Estimates reflect a consensus of sell-side analyst estimates, which may lag as market conditions change.

6. Earnings growth is the percentage change in a firm's earnings per share (EPS) in a period, as compared with the same period from the previous year.

7. Earnings before interest and taxes (EBIT) measures a company's net income before income tax and interest expenses are deducted. Also known as operating income, EBIT is used to analyse the performance of a company's core operations.

8. Standard deviation is a measure of how dispersed the data is in relation to the mean. Low, or small, standard deviation indicates data is clustered tightly around the mean, and high, or large, standard deviation indicates data is more spread out.

9. The MSCI ACWI ex USA Value Index captures large- and mid-cap securities exhibiting overall value style characteristics across developed and emerging markets countries, excluding the United States. The value investment style characteristics for index construction are defined using three variables: book value to price, 12-month forward earnings to price, and dividend yield. The MSCI ACWI ex USA Growth Index captures large- and mid-cap securities exhibiting overall value style characteristics across developed and emerging markets countries, excluding the United States. The growth investment style characteristics for index construction are defined using five variables: long-term forward EPS growth rate, short-term forward EPS growth rate, current internal growth rate, long-term historical EPS growth trend, and long-term historical sales per share growth trend.