You'll be re-directed to the Institutional Investor site.

Key Takeaways

- Emerging market equities offer exposure to fast-growing economies and key drivers of global growth. Many companies in developing markets are relatively inexpensive compared to their developed market peers.

- Investing in a wide range of emerging market stocks, both household names and lesser-known small- and mid-cap securities, gives investors broad diversification and the potential to generate alpha.1

- Over the past two decades, a portfolio with a blend of the MSCI Emerging Markets Index and the MSCI World Index (developed market equities) would have generated higher risk-adjusted returns than a portfolio comprised of only the MSCI World Index.2

- The Dodge & Cox Emerging Markets Stock Fund, with its valuation discipline and focus on individual companies around the globe and across the entire market capitalization3 spectrum, is well positioned to capitalize on the investment opportunities emerging markets offer.

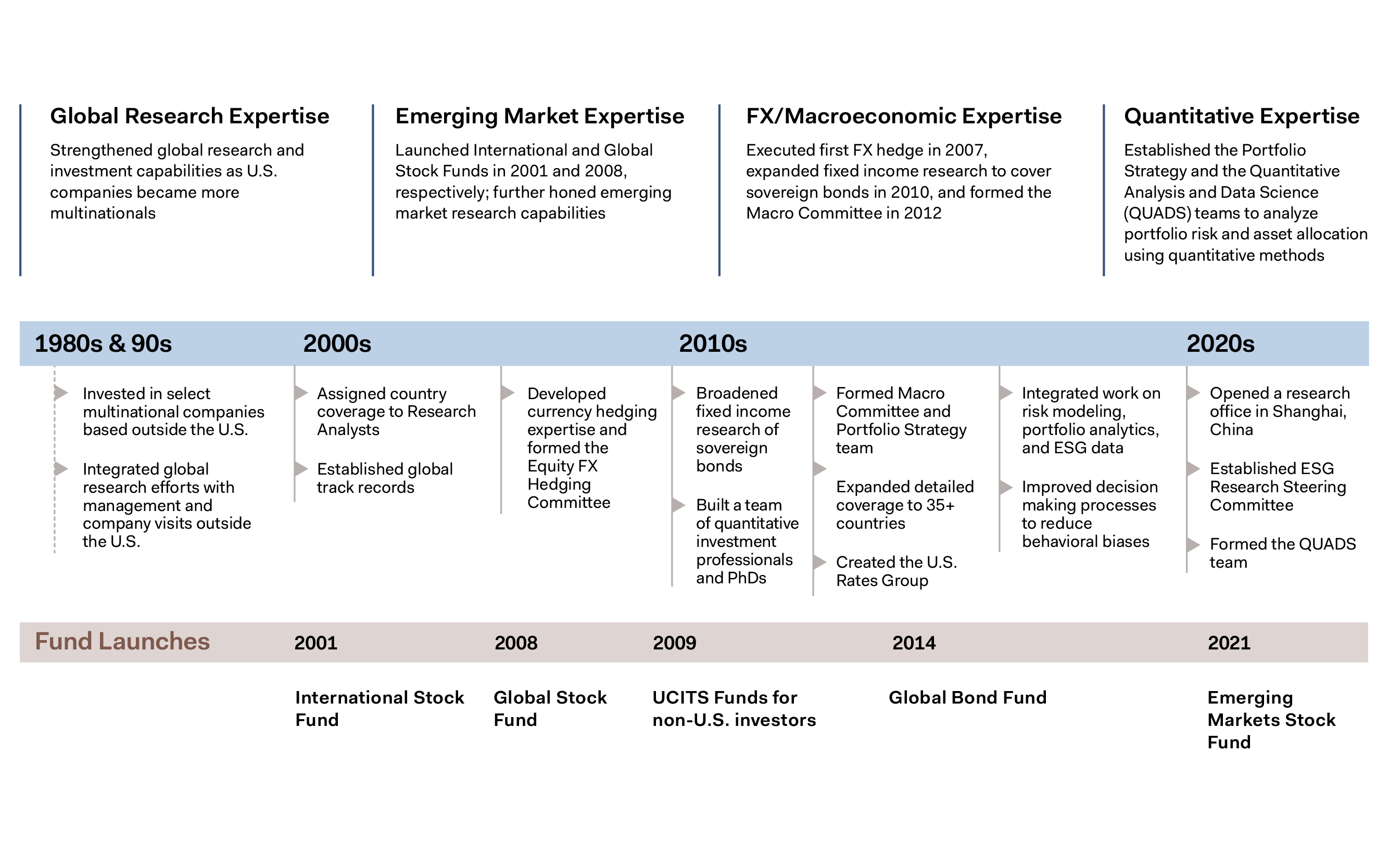

Over the past 40 years, investors have followed the rise of emerging market economies like China and the emergence of global leaders like Taiwan Semiconductor Manufacturing, Tencent, Samsung Electronics, and Alibaba.4 While these companies have become emerging market success stories, many investors may not fully appreciate the breadth of investment opportunities across the developing world. Emerging market businesses—many of them are smaller companies that are not well known outside their home markets—are exposed to powerful economic tailwinds, creating a plethora of potential investment targets.

Our enthusiasm for these opportunities, combined with our global research and deep knowledge of companies across industries, prompted us to create the Dodge & Cox Emerging Markets Stock Fund, the seventh fund we have launched in our firm’s 93-year history. We believe our time-tested, long-term, bottom-up, value-oriented approach is well suited for the challenges and opportunities presented by the emerging markets. We will talk about the Fund later in this paper. To start, we will focus on the emerging markets themselves and what makes them so compelling to us as investors.

Compelling Growth Opportunities

Emerging markets comprise over 80 percent of the world’s population and are responsible for nearly 80 percent of global gross domestic product5 (GDP) growth. Due to its economic success over the last 40 years, China is now the world’s second-largest economy. Going forward, dozens of other emerging market countries are showing impressive growth and have the potential to also expand rapidly. Many such countries are benefiting from advances in education and technology, the adoption of more market-friendly policies, positive demographic trends, and rising urbanization. Latin America and Southeast Asian countries are also poised to benefit from the nearshoring6 and friendshoring7 of the global supply chain. This growth story translates into opportunities for companies located or doing business in these markets.

Compared to their developed market peers, many emerging market companies have the potential to increase earnings at a faster rate due to increasing living standards in their domestic markets and rising demand from the rest of the world. That is not to say investing in emerging market companies comes without risks. Many emerging market countries face notable challenges, such as underdeveloped and less resilient economies, greater political instability, and less well-established and predictable legal and regulatory regimes. Emerging market investors may also have less access to reliable, publicly available information about companies. Furthermore, emerging markets suffered disproportionately during the COVID-19 pandemic. However, many emerging economies have since recovered more quickly than some of their developed peers and are now in a better fiscal situation compared to past crises.

Figure 1: Emerging Market Companies Are Relatively Inexpensive11

Source: MSCI, S&P.

Figure 2: Earnings per Share (EPS) Long-Term Growth Rate12

Source: FactSet, MSCI, S&P.

As a group, emerging market companies have lower valuations and higher earnings growth8 than their developed market counterparts (see Figures 1 and 2). Over the past 20 years, the aggregate market value of emerging market companies as a percentage of total global equity market capitalization has more than doubled (see Figure 3). This shows how quickly emerging markets are growing relative to developed markets and how much the emerging market investable universe has expanded. In 2001, the total market value of the stocks in the MSCI Emerging Markets Index was equal to about 5 percent of the market cap of the MSCI ACWI (All Country World Index).9 That number is currently about 11 percent.10 In addition, companies that are based in emerging markets or largely serve emerging markets currently comprise approximately 30% of total global market cap.

Figure 3. The Emerging Market Investable Universe Has More Than Doubled Over the Past Two Decades

Source: MSCI.

Stock Selection Opportunities

We think of emerging market stocks in two broad categories: very large businesses (many of them household names) and a much longer list of small and mid-sized firms that the typical investor has never heard of (see Figure 4). By our count, there are thousands of investable companies in the emerging market universe.

Figure 4: Including Smaller Companies in the Investable Universe Allows for Greater Diversification

Source: MSCI.

One way to think about this split is by focusing on some of the key engines of global growth. Consider the global digital supply chain that underpins our lives. At one end of the spectrum is Taiwan Semiconductor Manufacturing, one of the world’s largest companies, with a market cap of more than $421 billion. At the other end are Yageo ($7 billion market cap), Nanya Technology ($6 billion), and Powertech Technology ($2 billion), other Taiwanese businesses that manufacture and distribute electronic components. This is a small sample of emerging market opportunities, but the larger point is that the growth of the global supply chain plays a role in the potential success of these smaller companies. We see the same pattern in other factors driving global economic growth—commodity production, e-commerce, and increased penetration of financial products. Emerging market companies of all sizes are providing goods and services the world demands.

Since large-cap emerging market companies are mostly concentrated in the Information Technology and Financials sectors, investors need to be willing to invest in small- and mid-cap companies to achieve broad diversification in emerging markets. Not every emerging market investment will succeed, and finding the hidden gems in the small- and mid-cap world is not simple or straightforward. It requires extensive research and a global reach. But for those with the capabilities, the potential rewards are large. Put another way, we believe the emerging markets are an ideal place for active managers to perform their craft.

Diversification Benefits to Investors

Emerging market equities offer unique opportunities and risks that may complement a diversified portfolio. Investing in emerging markets is typically considered riskier than investing in developed markets. Indeed, over the past two decades, the MSCI Emerging Markets Index has been more volatile than the MSCI World Index of developed market stocks, using the standard deviation14 of monthly returns as a proxy for volatility. Over the same period, the MSCI Emerging Markets Index generated higher returns than the MSCI World Index. That is not surprising. However, investors might be surprised to learn that, over the past two decades, a portfolio reflecting a blend of emerging and developed markets indices would have generated higher returns than a developed markets-only portfolio, with only a modest increase in volatility (see Figure 5, tracking the performance of various blends of the MSCI Emerging Markets and MSCI World Indices).

Figure 5: Exposure to Emerging Markets Has Historically Improved Risk-Adjusted Returns15

Source: Bloomberg, MSCI. Past performance is no guarantee of future results. Index returns include dividends, but unlike Fund returns, do not reflect fees or expenses.

Our Fund

We launched the Dodge & Cox Emerging Markets Stock Fund in May 2021 to offer investors a portfolio that includes the most compelling emerging market investment ideas identified by our global research team. We study a broad research universe of roughly 4,000 emerging market stocks across approximately 60 countries, including many emerging market companies that are not part of the Fund’s benchmark, the MSCI Emerging Markets Index.

We consider companies across the market capitalization spectrum. Fund holdings include companies based in emerging markets and companies based in developed markets with significant economic exposure to emerging markets.

Casting a wide net means we consider more companies, countries, and sectors than a typical emerging markets fund. Our portfolio includes many stocks that are not household names in the United States. While dozens of Wall Street analysts follow every Fortune 500 company, few analysts cover more than the largest of these emerging market companies. As of September 30, 2023, the Fund had 40 percent of its net assets in small- and mid-cap stocks.16 Many of these smaller-cap holdings have exposure to attractive growth drivers, such as increasing consumption patterns, demand for a broader suite of financial services, expanding telecommunications and internet coverage, and real estate development, to name a few. In some cases, there are no large-cap investment alternatives providing exposure to particular growth drivers. By expanding the universe of potential emerging market stocks to include smaller companies, the Fund’s shareholders get three benefits: 1) greater diversification through exposure to companies, sectors, and regions; 2) additional opportunities to generate alpha through investment in companies not included in commonly tracked indices; and, 3) risk diversification.

Approximately half of the Fund is comprised of smaller positions that are less than 50 basis points.17 Many of these holdings are lesser known small- and mid-cap stocks. Including these companies in our portfolio allows for greater diversification across regions and sectors for the Fund. While we rarely expect to see these smaller positions show up as top or bottom contributors, in aggregate they have contributed consistently to the portfolio's performance since the Fund's inception.

Like other Dodge & Cox Funds, this Fund has below-average fees and expenses compared to its peers. This Fund's net expense ratio is currently capped at 70 basis points18 versus a median of 96 basis points for actively managed funds within the Morningstar Diversified Emerging Markets category.19 That difference winds up in the pockets of our shareholders and makes a difference to performance over time.

The Fund is constructed based on Dodge & Cox’s strict valuation discipline and fundamental approach to stock selection, with a portfolio built on the expertise of our global industry analysts. In the years we have spent investing in emerging market companies for other Dodge & Cox mutual funds, we have built tools to enhance our analysts’ ability to identify risks and opportunities in emerging markets. In managing the portfolio, the Emerging Markets Equity Investment Committee also relies upon the breadth of our equity and fixed income research teams. This includes our Macro Analysts who identify the geopolitical and institutional risks that disproportionately affect emerging market currencies and capital markets.

In Closing

As an active manager, the Dodge & Cox Emerging Markets Stock Fund gives us the flexibility to pursue the opportunities we see as most compelling across the developing world. Investors who share our long-term horizon and want exposure to value-oriented companies in difficult-to-access emerging markets should consider our Fund. We look forward to discussing this investment opportunity with you.

Continuously Evolving Our Investment Capabilities

Authors

Disclosures

Before investing in any Dodge & Cox Fund, you should carefully consider the Fund’s investment objectives, risks, and charges and expenses. To obtain a Fund’s prospectus and summary prospectus, which contain this and other important information, or for current month-end performance figures, visit dodgeandcox.com or call 800- 621-3979. Please read the prospectus and summary prospectus carefully before investing.

The information provided is not a complete analysis of every material fact concerning any market, industry or investment. Data has been obtained from sources considered reliable, but Dodge & Cox makes no representations as to the completeness or accuracy of such information. The information provided is historical and does not predict future results or profitability. This is not a recommendation to buy, sell, or hold any security and is not indicative of Dodge & Cox’s current or future trading activity. Any securities identified are subject to change without notice and do not represent a Fund’s entire holdings. Dodge & Cox does not guarantee the future performance of any account (including Dodge & Cox Funds) or any specific level of performance, the success of any investment decision or strategy that Dodge & Cox may use, or the success of Dodge & Cox’s overall management of an account.

The Dodge & Cox Emerging Markets Stock Fund invests in securities and other instruments whose market values fluctuate within a wide range so your investment may be worth more or less than its original cost. International investing involves more risk than investing in the U.S. alone, including currency risk and a greater risk of political and/or economic instability; these risks are heightened in emerging markets. The Fund may use derivatives to create or hedge investment exposure, which may involve additional and/or greater risks than investing in securities, including more liquidity risk and the risk of a counterparty default. Some derivatives create leverage.

Dodge & Cox Funds are distributed by Foreside Fund Services, LLC, which is not affiliated with Dodge & Cox.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed, or produced by MSCI.

Endnotes

1 Alpha is a measure of performance and indicates whether an investment has outperformed the market return or other benchmark over some period. Positive alpha means that the investment’s return was above that of the benchmark.

2 The MSCI Emerging Markets Index captures large- and mid-cap representation across emerging market countries. The MSCI World Index is a broad-based, unmanaged equity market index aggregated from developed market country indices, including the United States. It covers approximately 85% of the free float-adjusted market capitalization in each country.

3 Market capitalization is a measure of the security’s size. It is the market price of a security multiplied by the number of shares outstanding.

4 As of September 30, 2023, Taiwan Semiconductor Manufacturing, Tencent Holdings, Samsung Electronics, and Alibaba Group Holdings were the largest companies in the MSCI Emerging Markets Index.

5 Gross domestic product (GDP) measures the monetary value of final goods and services—those that are bought by the final user—produced in a country in a given period of time. It counts all of the output generated within the borders of a country. GDP is composed of goods and services produced for sale in the market and also includes some non-market production, such as defense or education services provided by the government.

6 Nearshoring in the supply chain refers to the practice of outsourcing business processes or services to companies located in neighboring countries.

7 Friendshoring (also known as allyshoring) is the act of manufacturing and sourcing from countries that are geopolitical allies.

8 Earnings growth is the percentage change in a firm's earnings per share (EPS) in a period, as compared with the same period from the previous year.

9 The MSCI ACWI (All Country World Index) Index is a broad-based, unmanaged equity market index aggregated from developed market and emerging market country indices.

10 Unless otherwise specified, weightings and characteristics are as of September 30, 2023.

11 Price-to-earnings (forward) ratios are calculated using 12-month forward earnings estimates from third-party sources as of the reporting period. Estimates reflect a consensus of sell-side analyst estimates, which may lag as market conditions change. MSCI’s official forward price-to-earnings ratio data is available since June 30, 2003. The MSCI EAFE (Europe, Australasia, Far East) Index is a broad-based, unmanaged equity market index aggregated from developed market country indices, excluding the United States and Canada. It covers approximately 85% of the free float-adjusted market capitalization in each country. The S&P 500 Index is a market capitalization-weighted index of 500 large-capitalization stocks commonly used to represent the U.S. equity market.

12 Calculated using FactSet Market Aggregates' EPS Long-Term Growth Rate formula, which aggregates the individual constituent's long-term growth rate available for any given period. The universe of companies in this calculation is limited to those with available EPS long-term growth estimate coverage.

13 The chart shows the top ten constituents in the MSCI Emerging Markets Index as of September 30, 2023.

14 Standard deviation measures the volatility of the returns. Higher Standard Deviation represents higher volatility.

15 Performance data for the MSCI Emerging Markets Net Total Return USD Index is first available in Bloomberg starting on December 31, 1998. As a result, the first annual period of performance begins on December 31, 1999.

16 Defined as under $10 billion in market cap.

17 One basis point is equal to 1/100th of 1%.

18 The Fund’s gross expense ratio is 1.24% and net expense ratio is 0.70%. Dodge & Cox has contractually agreed to reimburse the Fund for all ordinary expenses to the extent necessary to maintain Total Annual Fund Operating Expenses at 0.70% until April 30, 2026. This agreement cannot be terminated prior to April 30, 2026 other than by resolution of the Fund’s Board of Trustees. For purposes of the foregoing, ordinary expenses shall not include nonrecurring shareholder account fees, fees and expenses associated with Fund shareholder meetings, fees on portfolio transactions such as exchange fees, dividends and interest on short positions, fees and expenses of pooled investment vehicles that are held by the Fund, interest expenses and other fees and expenses related to any borrowings, taxes, brokerage fees and commissions and other costs and expenses relating to the acquisition and disposition of Fund investments, other expenditures which are capitalized in accordance with generally accepted accounting principles, and other non-routine expenses or extraordinary expenses not incurred in the ordinary course of the Fund’s business, such as litigation expenses. The term of the agreement will automatically renew for subsequent three-year terms unless terminated with at least 30 days’ written notice by either party prior to the end of the then-current term. The agreement does not permit Dodge & Cox to recoup any fees waived or payments made to the Fund for a prior year.

19 Median of the lowest cost share class prospectus net expense ratio for U.S. domiciled funds within the Morningstar Diversified Emerging Markets category (excluding index, enhanced index, and fund of funds). Source: Morningstar Direct (data as of September 30, 2023; downloaded on November 15, 2023). © 2023 Morningstar.